KSeF 2026 is no longer just for accounting. It's an IT project that will touch every stage of issuing and receiving invoices. Instead of paper and PDF, we're introducing XML-structured invoices based on the FA(3) schema, communication via the KSeF API, new certificates, and offline modes. It sounds technical, but the gist is simple: if a company's systems don't communicate with KSeF, sales and billing can come to a standstill. This text is a practical guide on how to prepare the infrastructure and processes for a safe and efficient transition.

What does this mean in practice for you and your team? Verifying where invoices are generated within the company and whether the software can generate the correct invoice (3). Planning ERP integration with the National e-Invoice System API, including buffers and queues in case of interruptions. Organizing authorizations and certificates so that only the right people can sign and send documents. Defining new workflow procedures, creating visualizations for contractors, and short training sessions for sales, administration, and accounting. This can be done even in a smaller company if you start methodically and step by step.

Every day, we support dozens of accounting firms and manufacturing companies with KSeF migrations, ERP integrations, and invoice management. We've gathered experience from implementations and testing to provide you with specific guidance instead of generalities. We'll show you what to watch out for, what can be done immediately, and what requires planning and short tests. If you want to navigate KSeF 2026 smoothly and without downtime, start with a few simple IT decisions.

Timeline: Key Implementation and Tool Dates

Below is a practical roadmap for KSeF 2.0 from an IT perspective. We've compiled only those milestones that have a real impact on integration, authorizations, and team performance.

September 1, 2025

disabling test and DEMO environments KSeF 1.0. New test registrations only in KSeF 2.0.

September 1, 2025September 30, 2025

start of open tests KSeF 2.0 API for suppliers and companies. A good time to start integration scenarios and FA(3) validations.

September 30, 2025October 15, 2025

possibility of integration via API with pre-production environment (DEMO)Use for dry testing before go-live.

October 15, 2025November 1, 2025

start MCU (Certificate and Authorization Module)From this day on, you can grant permissions and apply for KSeF certificates.

November 1, 2025November 2025

KSeF 2.0 Taxpayer Application in a test version for entrepreneurs to get to know the functions and flows before the obligation.

November 2025January 26-31, 2026

technical break between KSeF 1.0 and 2.0. Plan for a change window and deployment freeze.

January 26-31, 2026February 1, 2026

production start KSeF 2.0. Valid FA(3) (replaces FA(2)); authentication possible KSeF certificate; the original invoice is XML file in KSeF, and PDF/paper is only a visualization. Modes offline/offline24 require markings QR codes.

February 1, 2026April 1, 2026

the second stage of the KSeF obligation for other taxpayers (except the smallest "digitally excluded").

April 1, 2026December 31, 2026

end tokensFrom 2027 onwards, in practice, they will be KSeF certificates.

December 31, 2026January 1, 2027

an obligation for the smallest "digitally excluded" taxpayers (including low value of a single invoice and monthly sales).

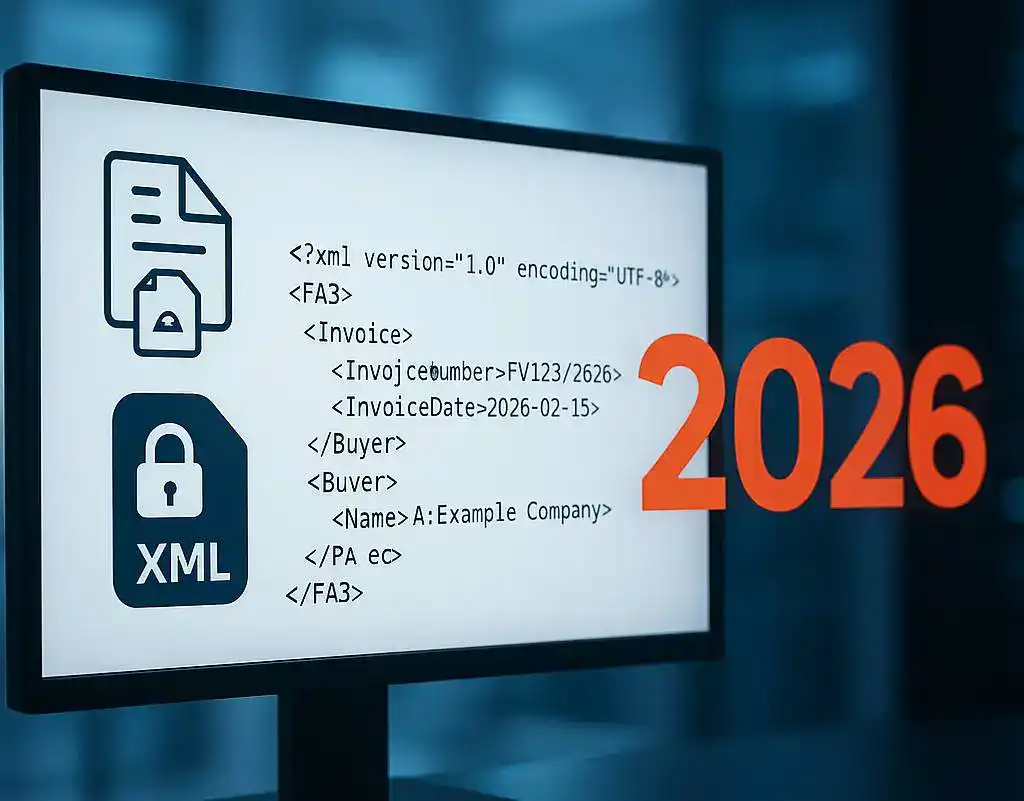

January 1, 2027FA(3) new structured invoice schema (XML)

FA(3) is the target, effective from February 1, 2026 e-invoice structure in KSeF. FA(2) remains in circulation until January 31, 2026, and from February 1, all structured invoices, including corrections and final invoices relating to documents issued before that date, are issued in FA(3). The original invoice is the XML file sent and accepted in KSeF, not a PDF or printout. The specifications and announcements were published by the Ministry of Finance.

What does FA(3) consist of?

The FA(3) main diagram includes the following sections: Header, Entity1, Entity2, Entity3, Authorized Entity, Fa, Footer, Attachment. Elements obligatory are Headline, Subject1, Subject2 and Fa. Elements optional is Subject3, Footer and Attachment, and optional is the Authorized Entity. The MF brochure describes in detail the content of each section and indicates which fields are mandatory and which are not.

Key rules that influence integration

Format and validation

A file is always XML, compliant with the XSD provided by the Ministry of Finance. Validation includes both schema rules and semantic rules described in the documentation and brochures. Current XSD files and examples can be found in the official knowledge base National e-Invoice System.Taxpayer identification

The buyer's Tax Identification Number is entered only in the field Tax Identification Number in the element Entity2/IdentificationDataEntering it in the VAT number or ID number will prevent the buyer from properly sharing the invoice in KSeF. This is a common error when migrating from FA(2).Header and versioning

The header contains fields such as: FormCode and FormVariantIn FA(3) the brochure indicates the FA system code with variant 3 and the schema version attribute, and DateOfManufactureFa given in UTC. The production date may differ from the sale date in field P_1 and from the date of actual submission to KSeF. This is important for time compliance and auditing.Continuity of settlements

As of February 1, 2026, corrections and final invoices are issued on FA(3) even if the original invoice was previously created on FA(2). Integrations must take this relationship into account when linking documents and reporting.

What actually changes FA(3) with respect to FA(2)

• Unification and clarification of fields based on consultations with businesses and system providers. In practice, this means fewer uncertainties when mapping data and clearer rules for identifying pages and positions.

• Extended implementation instructions in MF brochures, including explicit indication of places for identification and address data and detailed descriptions of the Fa and Footer sections.

• Attachment as a tool for transmitting complex positional data and units of measurement, which facilitates the representation of heterogeneous product catalogs.

• Clear rules for the buyer's VAT number in the context of providing an invoice, which removes a typical cause of errors with FA(2).

Listing modes: online, offline, offline24, failure

Online (standard)

• Issuing and immediate sending of an XML file (FA(3)) to KSeF via API or Taxpayer Application.

• The KSeF number is assigned automatically and returned to the UPO; it is the basis for document identification.

Offline24 (KSeF available, invoice outside the system)

• Issuance of an e-invoice outside KSeF and the obligation to send it no later than the next business day after issuance.

• The visualization for the buyer must contain two QR codes: "OFFLINE" (access and verification) and "CERTIFICATE" (issuer's identity) - requires a KSeF certificate.

• The date of issue is P_1 in FA(3); the date of receipt in B2B is generally the moment of assigning the KSeF number.

Offline (KSeF announced unavailability)

• Used only when the Ministry of Finance announces a system unavailability in the Public Information Bulletin (BIP). Invoices are issued outside the KSeF and sent no later than the next business day after the unavailability ends.

• The visualization requires two QR codes (OFFLINE and CERTIFICATE); generating the second requires a KSeF certificate. Date rules are the same as in Offline24.

Failure (declared KSeF fault) and total failure

• Failure: invoices should be issued outside KSeF, sent within 7 business days of the end of the failure; visualization with two QR codes (OFFLINE and CERTIFICATE).

• Total failure: extraordinary situations; paper or e-invoice is issued outside KSeF, there is no obligation to send documents after the failure; no QR codes.

Authentication and security

From November 1, 2025, entrepreneurs will be able to use KSeF certificates, which will become the primary method of authenticating and signing invoices. The certificate is required, among others, in offline and offline24 modes to generate the "CERTIFICATE" QR code. authorization tokens remain in use only until December 31, 2026, so it is worth planning the migration in 2025.

Access management is carried out by MCU (Certificate and Authorization Module)This is where user permissions are assigned and certificates are downloaded. Implementing a consistent access policy – with role separation and regular review – is crucial for security and minimizing the risk of abuse.

In practice, certificates and private keys should be stored in secure repositories, such as HSMs or secret managers with access control. It's also worth ensuring that all UPOs and integration logs are rotated and archived every few months. This not only meets formal requirements but also facilitates rapid recovery of business continuity in the event of an incident.

Integration with ERP and FK: architecture and best practices

Implementing KSeF requires adapting ERP and financial and accounting systems to handle FA(3) structured invoices. The most important steps are ensuring data compatibility, seamless communication with the KSeF 2.0 API, and secure document transfer. Integration testing can begin on September 30, 2025, in an environment provided by the Ministry of Finance, allowing several months of preparation before the requirement comes into effect.

Integration architecture may look different depending on the size of the company:

• in popular ERP systems (e.g. Comarch, enova, SAP, Dynamics) manufacturers prepare their own connectors,

• in companies with distributed applications, the integration layer (ESB, iPaaS) works well,

• smaller entities can use the Taxpayer Application or e-microcompany instead of full integration.

Good technical practices These include buffering and queuing invoices to prevent them from getting lost during downtime, validating XML data before submission, and logging communications with KSeF for audit purposes. It's also crucial to manage the entire cycle—from issuance and receipt to corrections and duplicates—and ensuring transparent statuses in the ERP so the accounting department has immediate insight into whether an invoice has been accepted.

Internal processes: processes, document flow and training

The National e-Invoice System is transforming not only software but also the daily work of accounting, sales, and administration departments. The invoice in XML FA(3) format becomes the sole source document, while PDF or paper invoices can only serve as visualizations for the customer. Therefore, adapting procedures and document flow within the company is crucial.

New procedures These should include: issuing structured invoices, supporting offline/offline24 modes with the requirement to submit the document to the KSeF (National Securities and Exchange Office), generating visualizations with QR codes, and storing local copies of XML and UPO invoices as accounting documents. A clear division of responsibilities between departments is also necessary – who is responsible for issuing invoices, who for shipping, and who for monitoring statuses.

Document circulation requires updating so that buyers without access to KSeF (e.g., foreign contractors) can receive the correct invoice visualization. It's also worth implementing integration log and XML backup archiving in the event of an audit or failure.

Employee training are essential for every department to understand the new process. Accounting must understand the difference between XML and visualization, sales must understand how to submit invoices to clients, and IT must understand how to manage emergency procedures. The Ministry announces that the beginning of 2026 will be a training period, allowing for a gradual implementation of changes, but the sooner a company prepares its employees, the lower the risk of chaos.

Compliance and exceptions: what's not yet in KSeF and transition periods

Although KSeF will become mandatory for most companies from 2026, not all invoicing is subject to its requirements. The Ministry of Finance has provided for exceptions and transitional periods that should be considered in the processes.

Exclusions from KSeF These include, among others, fiscal receipts with a Tax Identification Number (NIP) up to PLN 450 (so-called simplified invoices), B2C sales to consumers, and some transactions with foreign contractors. In such situations, invoices may still be transferred outside the National Tax and Customs Securities Fund (KSeF), although it is recommended to use uniform procedures for archiving and transmitting documents in visual form.

Transitional periods:

• February 1, 2026 – start of the obligation for large taxpayers,

• April 1, 2026 – the obligation extends to other companies,

• January 1, 2027 – the smallest “digitally excluded” entrepreneurs join in the last stage.

It is also worth remembering that authorization tokens can be used in parallel with KSeF certificates only until the end of 2026 – from 2027 only the certificate will remain.

In practice, this means that in 2026, companies must maintain a dual regime: processing invoices in the KSeF system, but also having procedures in place for documents issued outside the system. Clear instructions, a clear division of responsibilities, and an updated archiving policy will help avoid misunderstandings during this period.

Impact on finance and administration: costs, risks, business continuity

Implementing KSeF is not just a technical project; it also directly impacts costs and administrative workflow. Companies must factor in expenses for updating ERP and accounting systems, implementing API integration, purchasing certificates, and training employees. Additionally, there are organizational costs, such as developing new document flow procedures and XML archiving.

The biggest risk is the loss of invoicing continuity – incorrect data mapping, lack of FA(3) support in the system, or offline issues can result in delays in sales and accounting. Failure protection is also crucial – shipping queues, return procedures, and status monitoring should be standard.

A well-planned implementation, however, offers benefits: faster document flow, a uniform invoicing standard, and easier tax audits. We provide daily support to accounting firms preparing for the regulatory changes of February 1, 2026. We help them with issues such as ERP integration, certificate configuration, employee training, and day-to-day IT issues. If you want to navigate this transition smoothly and cost-effectively, get in touch – we'll help you prepare your system and team so that February 1, 2026, is a workday like any other.

Frequently asked questions

When will KSeF be mandatory?

Can I still send invoices in PDF?

When can I start testing integration with KSeF?

What is FA(3)?

What is the difference between a token and a KSeF certificate?

How do offline and offline24 modes work?

Is employee training needed?

Will there be sanctions for errors in 2026?

KSeF 2026 is the biggest change in invoicing in years – replacing paper and PDF documents with a single, structured XML file compliant with the FA(3) schema. Implementing this system requires not only updating financial and accounting software, but also new procedures, authentication certificates, integration testing, and employee training.

However, a well-executed process offers significant advantages: unified document flow, enhanced data security, and full regulatory compliance. It's crucial to start preparing early: API testing in fall 2025, certificate configuration in November, and operational readiness in February 2026.

If your company is facing the challenge of implementing KSeF, don't wait until the last minute. Every week is an opportunity to calmly prepare your systems and employees. Take advantage of our experience – we'll show you how to navigate the changes step by step, without the risk of downtime and additional costs.